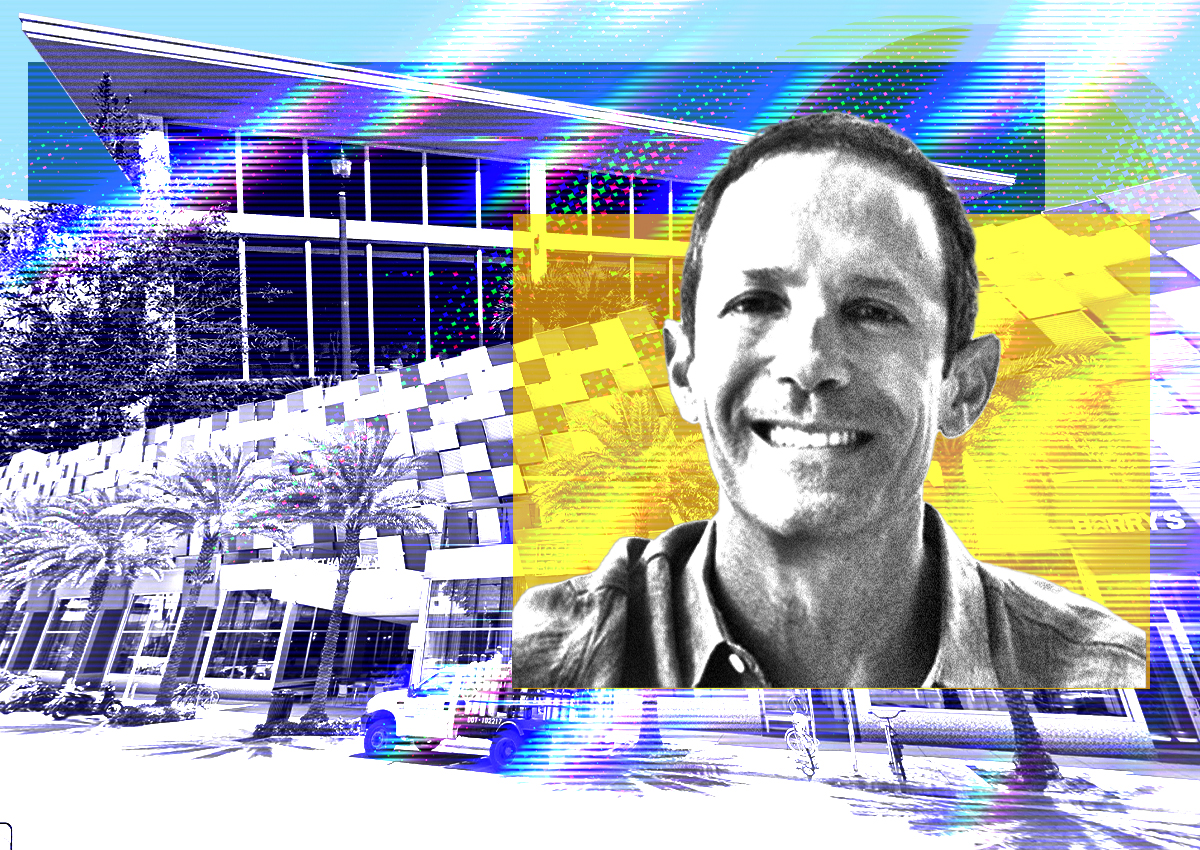

Nightingale’s head of acquisitions is leaving as his former firm faces allegations of misappropriating funds related to two large office investments.

Will Hutton posted on LinkedIn yesterday that he had left the company led by Elie Schwartz.after the post appears real deal An independent manager appointed by investors on the crowdfunding site CrowdStreet accused Nightingale of embezzling tens of millions of dollars set aside for properties in Atlanta and Miami, reports Friday said.

“After nearly eight years at Nightingale Estate, I am embarking on a new journey,” Hutton wrote on his profile. “Thank you for your understanding and continued support during this transition.”

Neither Hutton nor Nightingale responded to requests for comment.

Hutton, a native of Wichita, Kansas, joined Nightingale in 2016 as an analyst at Cohen Equities and was later promoted to director of acquisitions and capital markets, deploying more than $2 billion in equity along the way, according to his LinkedIn page.

During that time, the company made some mega-deals, such as its $328 million purchase of Philadelphia’s 1.7 million-square-foot Center Square office tower, its $909 million purchase (and subsequent flip) of the Coca-Cola Building at 711 Fifth Avenue, and its $395 million purchase of 111 Wall Street and the land beneath it.

In 2019, Nightingale bought an 82,000-square-foot new office building in Soho for about $125 million and signed a lease with Microsoft. A year later, amid the pandemic, it bought the historic Whale Building in Brooklyn from Madison Realty Capital for $84 million.

Nightingale’s office properties have been in trouble for the past few months. The company’s Whale Building, Center Square complex and Soho office building are facing foreclosure.

The company’s biggest controversy, however, has been two deals it funded through crowdfunding platform CrowdStreet. The company raised $54 million to fund its planned purchase of the 1 million-square-foot Atlanta Financial Center, which it agreed to buy last year for $182 million.

The firm also raised $9 million to invest in the 110,000-square-foot Lincoln Square office building at 1601 Washington Boulevard in Miami Beach, which it bought for $80 million in 2016.

Both deals fell through.

The entities set up for those investments filed for bankruptcy on Friday, and their accounts are largely empty.

Most of the money was transferred to Schwartz and his affiliates almost immediately after the fundraising, Anna Phillips, an independent manager representing investors, said Friday.

“On top of that, the funds raised by both entities were misappropriated,” she said.